This is about 13k words long! Feel free to print or download it to your Remarkable / Kindle Scribe / iPad for easier reading.

About this essay: This is the first chapter of a book I am writing on Product Market Fit or PMF. This chapter, Understanding PMF, starts out by setting context for why PMF matters to early stage startups. It then lays out a definition for PMF – that it is a combination of two fits, PPF and MMF. It explains this through two case studies, one a success, and the other a failure. It then dives deeper into these two fits, and concludes with what the founder’s role in PMF, as well as come caveats and thumbrules for the founder to keep in mind. By the end of the chapter, the reader should have a broader understanding of PMF, the two fits, as well as a broad playbook for iterating to PMF.

Note to the reader: The term Product Market Fit is written in one of three ways: Product / Market Fit, Product-Market Fit, or Product Market Fit. I prefer the last. That said, given that the term is popularly abbreviated to PMF, that is indeed what I have used here in this piece, in almost all cases. Still, whenever I have needed to use the expanded term I have stuck to Product Market Fit, except when I quote writings where ‘Product/Market Fit’ or ‘Product-Market Fit’ has been used. Here I have stuck to what the original writers preferred.

1A/ Why Product Market Fit matters

1A.1/ Lack of Product Market Fit is the single biggest cause of startup failure

Most startups fail. Startup Genome, which evaluates and ranks global startup ecosystems, did a detailed study of 3,000+ high growth tech startups and estimated that 90% of these startups failed. Of these, they found that three-fourths failed due to premature scaling, i.e., where the startup invests in growth ahead of a proven and viable business model. The report said: “Startups that try to scale before they have reached product/market fit and streamlined their customer acquisition process don’t do very well.” Another study, by startup postmortem site Failory estimated that the biggest reason for startup failure, accounting for just over a third of failures, was the inability to achieve product market fit, stating failed startups “invest a lot of time and resources before you are confident people want what you are offering.”

Studies such as the above as well as multiple others by the likes of CB Insights, Autopsy etc., identify the lack of Product Market Fit (PMF hereonwards) as the key cause for startup failure. Founders recognise the importance of PMF too, reflected in tweets such as this by Sahil Lavingia, founder of creator commerce app Gumroad…

…or this by Robleh Jama, cofounder of Boom Vision app.

Clearly, PMF matters, for a) not achieving it is the single biggest cause of startup failure, and b) founders think it is mighty important too. So, what is PMF?

Well, PMF is notorious in that for long there has been no clear single universal definition. I have come across several definitions of PMF ranging from the extremely quantitative to the highly qualitative, like this from Marc Randolph, the Netflix cofounder, who puts it facetiously: “With apologies to Justice Potter Stewart, I’ve often felt that Product Market Fit is not unlike hard core pornography: hard to define, but you know it when you see it.” Fintech VC Sheel Mohnot has a similar though more family-friendly definition: “ I think it’s one of those things that’s like what is love? You know when you’re in love.”

The lack of a universal definition for PMF has always puzzled me, and also troubled me. Given that the achievement or lack of achievement of PMF is a critical factor in the success of the startup, not having a commonly agreed definition has always puzzled me. When you don’t have a clear definition, you also don’t have a clear idea of how to approach it and work towards it. Hence this attempt at setting out a definition for PMF that I hope will prove useful for founders.

1A.2/ VCs love PMF

Before we set out to define PMF, it is important to understand that it is a concept invented by Venture Capitalists (VCs) and not founders. It is a phrase that was popularised by Marc Andreessen of venture fund A16Z, who credited the invention of the term to Andy Rachleff, the cofounder of Benchmark. In that now infamous 2007 article, Marc wrote: “Lots of startups fail before product/market fit ever happens. My contention, in fact, is that they fail because they never get to product/market fit…The only thing that matters is getting to product/market fit. Product/market fit means being in a good market with a product that can satisfy that market.”

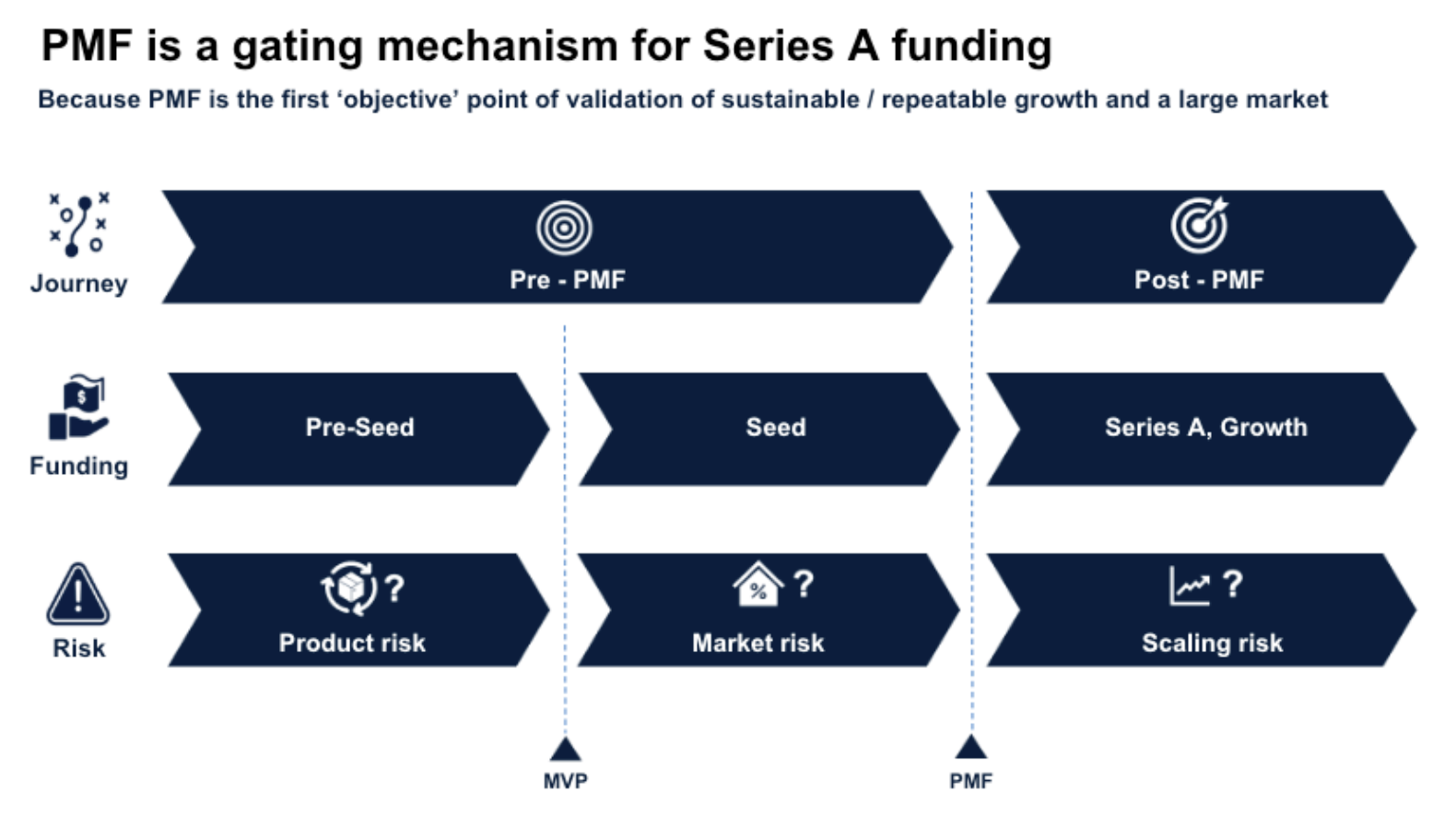

VCs love PMF because it serves as a convenient framework to evaluate a startup for funding. Evaluating a startup for PMF helps them understand where a startup is at, and whether the startup’s risk profile aligns with their investing strategy. Most VCs have a preferred stage at which they invest (there are certain multistage funds which invest across all stages of a startup’s life), and each stage corresponds to a certain kind of risk profile. The following graphic illustrates the stages and the risk being addressed at each stage.

To clarify:

- Pre-seed covers product development risk. This stage is where angel investors or friends and family come in (now you see MicroVCs also in this stage).

- After the product is ready and there is some early customer validation, the startup typically raises a seed round. The seed VC comes in here and helps cover market development risk. At this stage, there is proof that a market exists, and that there is a playbook to achieve it. This stage, where both product and market development risk is defrayed, is typically when the startup is considered to have achieved PMF by VCs.

- The final stage, post PMF, is the Series A+ stage going from early growth to late growth. Here the key risk is scaling risk. Capital here helps underwrite the risk of scaling to multiple channels or markets.

Effectively PMF is thus a gating device for VCs, specifically Series A and B VCs, who like to come into startups that have some degree of PMF. These days with buzzy startups, especially AI startups, a lot of these labels have started blurring. Preproduct startups get rounds larger than what Series B companies get, and so on. But the above staging / gating framework is a useful one to keep in mind, as the basis for the development and popularity of PMF, albeit led by the VCs. PMF matters to the Series A and beyond VCs because they need to make sure that before they invest more monies, that the startup has genuine and sustainable demand for their product. Else, they run the risk of pouring large sums of money into a company that may come a cropper. Signals of PMF provide some degree of assurance, and derisk the startup in the VC’s mind.

PMF alone doesn’t guarantee success. Startups with signs of PMF can later lose their way, but at the point of funding, signs of PMF give some comfort to the VC who is investing. Before you go big, you need to get it right. This is the signal that PMF provides, that the startup is headed in the right direction. It is how investors assure themselves of the genuineness of appeal or demand for the product as well as the playbook for growing it systematically. Post PMF, it effectively becomes a rinse and repeat strategy. PMF is effectively the nailing before the scaling.

PMF is thus doubly important. It is the single biggest early milestone in a startup’s journey. It is also vital to securing a Series A. But it doesn’t have a single agreed upon definition and playbook to achieve it. It is time to change that. In the next section, I present my definition of PMF.

1A/ TLDR

Most startups fail, not because they scale too slowly, but because they scale prematurely, before finding PMF. PMF is the single most critical milestone in a startup’s journey, and yet it remains loosely defined – part gut feeling, part data signal. That doesn’t seem right. It matters not just for the startup’s success, but also for funding. VCs popularised PMF, using it as a gating mechanism, helping them assess risk and determine when a startup is ready for funding. PMF is thus doubly important. Hence, this piece, where I set out to define it.

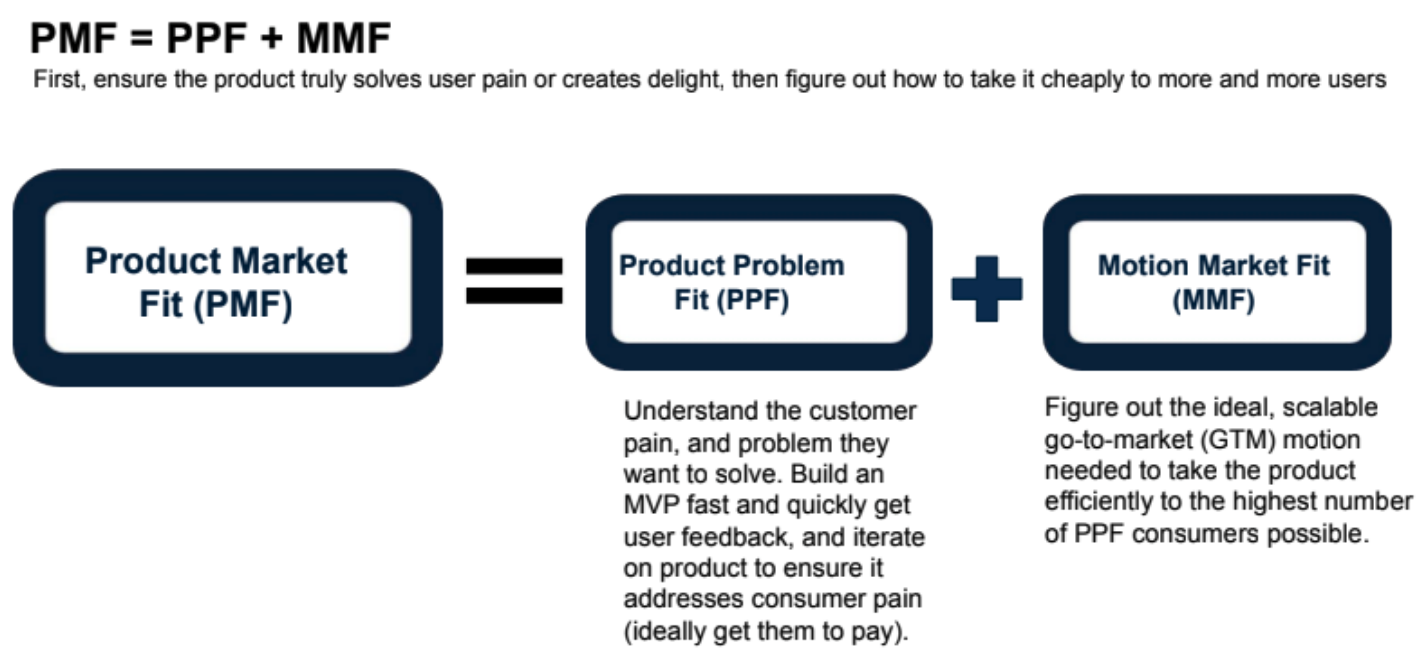

1B/ PMF = PPF + MMF

1B.1/ PMF is the achievement of two sequential fits

Given we learnt that PMF is achieved when you defray two risks, first, product development risk, and secondly, market validation risk, we can break PMF or Product Market Fit, into two sequential fits

- The first fit is Product to Problem Fit or PPF, where you validate that the product or solution that you created effectively solves the problem for a set of customers. Achieving this fit helps you defray product development risk.

- The second fit is Motion to Market Fit, or MMF. Motion is short for Go-To-Market (GTM) Motion. GTM or Go-To-Market consists of all of the activities required to efficiently market and sell your product to customers. By figuring out the right GTM Motion that helps you efficently capture and keep a large market, you are defraying market validation risk.

Thus, to achieve PMF, founders thus need to work through a 2-step process.

- First: achieve Product to Problem Fit, or PPF

- Next: work towards (GTM) Motion to Market Fit, or MMF

When you have PPF, and then MMF, you have achieved PMF.

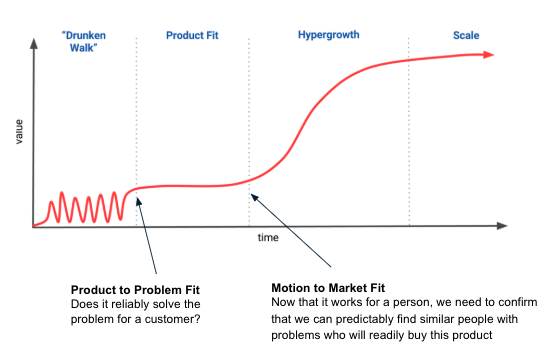

Here is a graphic illustrating the fits. The original graphic, on which I laid PPF and MMF legends, is from an article by Nikhyl Singhal.

To repeat, PMF can be defined as the sequential achievement of two fits, PPF and MMF. When you achieve PMF, you have a product that reliably solves the problem for a segment of customers, and you have an efficient motion to acquire more and more of these customers on a sustainable basis. In subsequent sections in this chapter, I will dive deeper into these two fits, PPF and MMF, including how to work towards them, as well as how to know if you have achieved them, i.e., the quantitative metrics and criteria to judge the achievement of these fits. Now, some nuances around PMF.

It is worth noting that there are business models such as media / gaming plays, and marketplaces, that have two-stage PMF. In these business models, you have to break PMF (and therefore PPF and MMF) into two phases. For instance in the media business, PMF has to be effected twice, first for user acquisition, as you capture customers through content, and then monetization when you sell the audience to advertisers. In the first stage, you have to showcase that you have a sustainable playbook to acquire and keep customers, i.e., achieve PMF on customer acquisition. In the second stage, you have to showcase that the acquired customers can be monetised on a sustained basis. For both these stages, PMF will in turn be split into PPF (product solves problem) and MMF (sustainable acquisition).

- First stage PMF = product solves problems for consumers, and you can sustainably acquire consumers and retain customers.

- Second stage PMF = product solves problems for advertisers, and you can sustainably acquire, and retain advertisers.

When it comes to marketplace businesses, there are two sides (buyers and sellers; users and providers etc). PMF is achieved when you have a playbook enabling sustainable acquisition on both sides, supported by strong unit economics. It is tough to go for PMF on both sides simultaneously. While founders should indeed put efforts to grow both sides, it is best to focus more efforts on the harder side. Typically, but not always, the harder side is supply (Drivers in Uber, Homes in Airbnb etc.). So focus on figuring out a repeatable plan for onboarding the harder side. Then make sure that the harder side is served by matching them with users from the easier side, and ensure monetisation. Again, for each of these sides, the PMF gets split into PPF (ensuring product love) and MMF (acquisition and retention).

To illustrate these two fits better, here are two case studies, one a B2B SaaS co that successfully achieved PMF, and the other a B2C smartwatch co that failed to achieve PMF. Through these case studies we will understand how startups navigate through the two fits to achieve, or fail to achieve PMF.

1B.2/ Front: a case study of successfully achieving PMF

Front is a great case study of how a startup can systematically work to achieve these two fits. Front was founded in 2013 as a shared email inbox for customer support teams, and was last valued at $1.7b in its Jun’22 Series D round. Front’s story offers several useful lessons for founders seeking and working towards PMF.

Getting to PPF:

- A narrow product with just the essential features: In the early days of Front, it was a barebones email client, with just two features, assigning (customer) mails to your colleagues and being able to comment internally on a mail. In fact, you couldn’t even add attachments. But it was enough for them to share with their beta customers, and get early feedback from. Mathilde Collin, the cofounder and then CEO spoke continuously to users to get their reactions, sensing what features customers were missing and getting Laurent Perrin, cofounder and CTO, to add the feature.

- The primary source of customer acquisition was the content that Mathilde was writing, centred around the themes of communication and email that resonated with their target audience. Over time, through content, and promoting to the YC network, they got to about 10 customers. But they were learning a lot from these early customers. They stuck with this routine for the first year. Mathilde: “Really the only things we did for the first year, at least, was just doing that. It was writing content, onboarding users, and building features. Every other distraction that you could think of, we didn’t do.”

- They hit strong PPF early with customer support teams: An early adopter set were support teams, who found Front to be a better way to interact with customers as it seemed more personal given it was email – hence, no tickets, no “reply above this line” etc. Given it was email it was also a lot more “intuitive to use”, and it was also easier for more people in the company to see support requests. Support teams were their initial wedge into organisations.

- Over time this initial set would expand beyond support teams to sales, recruiting, operations teams etc. Common to all of them, was the fact that they had a lot of emails coming in, and the team needed to collaborate on a reply or be aware of replies being made, or track progress on a specific customer etc. Front’s reason to exist, and thrive, started becoming more clear: “a lot of people inside the team need to handle these emails and they struggle managing that as a team because email wasn’t made for teams.”

Getting to MMF, and achieving PMF:

- Over time, the GTM playbook too became more crystallised, with strong organic inbounds thanks to word of mouth as well as a strong content engine. 70% of their 2015 leads were organic inbounds. Mathilde set up a team of SDRs to handle these inbounds. These content-led inbounds also led to a successful land and expand motions. Mathilde: “…so we always start with one tiny team at Tesla using it, but then another one and another one and another one.”

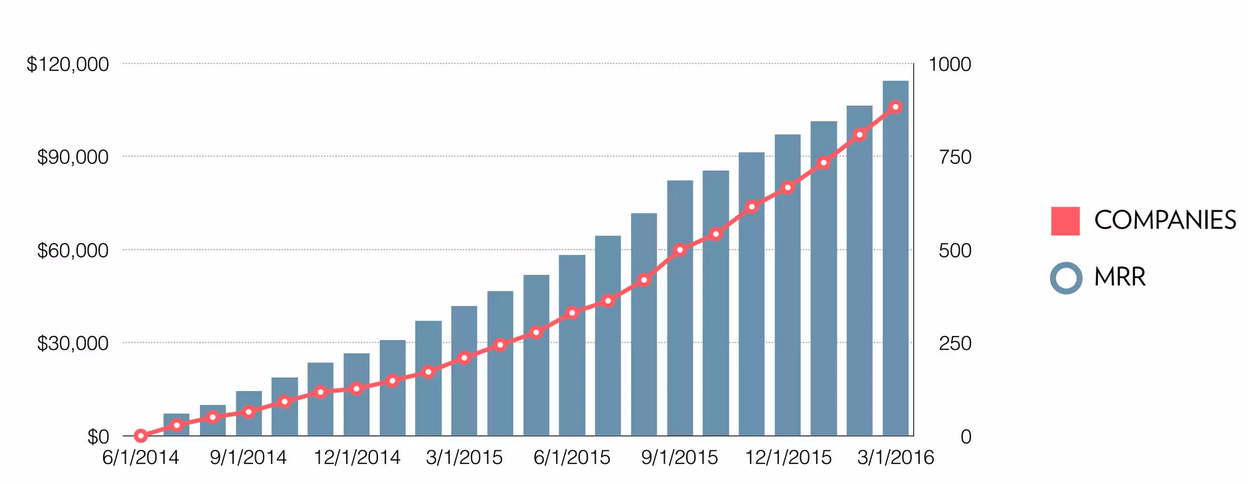

- The above chart is from Front’s Series A pitch deck where they raised $10m. By then (summer 2016), they had spent $1.3m to generate an ARR of $1.4m, they had close to 1,000 companies using it, and they had a strong land and expand motion. Mathilde: “on average, people spend 50% more after 12 months (net of churn)” and churn was around 3%.

- The strong Series A seemed a validation of Front having achieved product-market fit. Having nailed the product proposition and the go-to-market playbook, Front now had the capital to scale, and it did. The strong product-market fit it had achieved, and the continuing growth in users, revenue and metrics landed them a $66m Series B in December 2017, led by Sequoia.

The above case study is a text book example of how to achieve PMF; first, starting with a basic product that meets the core needs, while continuously speaking to users to get feedback and improve the product. Then having identified a core set of users, using them as a wedge to get into the company and doing a land and expand motion, all the while keeping the content-led playbook, their primary channel in the early years going.

1B.3/ Pebble: a case study in PMF failure

The smartwatch co Pebble is a classic case study of how a startup can achieve immense product love, and early traction, and thereby hit PPF, but eventually lose its way and fail. Founded in 2012, Pebble raised $43m across three Kickstarter campaigns as well as a $15m Series A from Charles River Ventures before declaring bankruptcy in late 2016. After seeing initial success in 2013 and 2014, it struggled to scale and expand, and as competition increased in the smartwatch industry, Pebble found itself caught in the middle without a clear positioning. A cash crunch following a bad Christmas quarter in 2015 led to financial stress and finally bankruptcy in late 2016. Pebble is a cautionary tale on how despite a strong fanbase and strong PPF, you can fail to achieve PMF.

Journey to PPF:

- Pebble launched in April 2012 on Kickstarter as an affordable e-paper display watch (see campaign pic below). Founder Eric Migicovsky built it to address a pain point he faced – that of wanting to access a message or alert without having to pull out his phone. The intentionally-designed product had immense battery life (7 days), was waterproof up to 40m. It did the basic notifications well – for missed calls, messages, meeting alerts, alarms. Via paired apps, and later through opening it up to developers, several other use cases opened up including fitness, navigation etc. It was a geek’s dream watch.

- Pebble’s April 2012 Kickstarter campaign’s runaway success put it on the map. They were looking to raise $100k but ended up raising $10.3m, becoming the most funded project in their history. The watches started shipping a year later after manufacturing issues delayed the release. By late 2013, they had sold 300,000 watches, and by late 2014 they clocked 1 million in sales. On the back of the buzz and sales, they saw a $15m Series A led by Charles River Ventures, to expand product range, and distribution channels.

- Pebble’s early GTM was focussed around generating PR and viral buzz, helped by the Kickstarter campaigns and developer outreaches. Over time a loyal community of fans and early adopters coalesced around the brand. It helped that Pebble listened to these users and often incorporated their feedback (the waterproof feature in fact was in response to user requests). This responsiveness, combined with product performance turned users into brand evangelists. It is fair to say that by end 2013 / early 2014, they had achieved PPF demonstrated by growing sales, a vibrant developer ecosystem, and a growing fan base.

Path to MMF, and challenges:

- With the new Series A capital, and a cohort of loyal fans, Pebble stepped up to invest in retail distribution channels such as Best Buy and AT&T stores. They launched their next iteration of products titled Pebble Steel, a more refined looking metal-inspired timepiece (see below). The product strength helped Pebble hold its own against competition, emerging as a strong #2 to the much older FitBit in the first quarter of 2014.

- In late 2014, Apple Watch launched, and anticipation about greater competition in the smartwatch / wearable market kept VCs from participating in Pebble’s Series B. As a result Pebble had to rely on debt, and another very successful Kickstarter campaign, where it raised $20m+. Going into 2015, sales continued to grow, but Pebble was beginning to be squeezed by Apple Watch from the top end offering a similar JTBD (job to be done) as Pebble, and Fitbit from the side, which had a sharper fitness-focused proposition. Pebble reacted by a push towards fitness features, and tried to go upmarket with Pebble Time in 2015, but these expansions – more models, more features – led to a loss of focus. Migicovsky said in a postmortem on Pebble: “We shifted from making something we knew people wanted, to making an ill-defined product that we hoped people wanted”.

- As Pebble pushed wider and upmarket, its limited marketing spend meant it couldn’t truly reach a wider audience, and thus expand its market. It had strengths and capabilities in marketing to developers, and leveraging the tech press, but winning in the mass market requires being able to leverage performance marketing and more mainstream marketing methods (GTM motion), and here Pebble was found wanting. As Eric Migicovsky put it: “Our marketing efforts (outside of the Kickstarter campaign) were pretty awful. We struggled with making strong decisions on marketing (and sticking to them) and wavered on hiring a head of marketing for years…” Effectively this meant that they couldn’t figure out a market or the (GTM) motion required to get there.

- By late 2015, Pebble had grown to 160 employees (from just 25 employees in 2013). From a profitable 2013, and breakeven 2014, Pebble was now in the red, as operating expenses rose, and margins slimmed; its gross margin dropped from 35% to 27% in 2015, due to competition, and a cost increase given SKU creep. Its margin of error was slim, and a weak last quarter in 2015 meant $15m in dead stock (on revenues of $81m in 2015), and a cash crunch which Eric says “we worked through the whole year (2016) to solve.” All numbers via Eric’s postmortem.

- The lack of venture funding post 2013, and the continuous need for working capital (despite the crowdfunding, it was perennially short of funds for expansion) meant Pebble was perennially short of money. This led it to raise debt, and this would prove its achilles heel, when growth came up short in 2015. As 2016 progressed, Pebble’s lender called in a loan which they couldn’t repay. While Eric tried to organise a fund raise (there was yet another Kickstarter campaign – this time they raised $13m) he finally had to declare bankruptcy in late 2016.

While Pebble got a lot right in the early days, and got a core set of early adopters / tech nerds to sign up and become buyers, it struggled to expand this product love to a wider base and the larger market. Competitive intensity clearly is a factor, but there were also some self-goals such as lack of clarity about the user, and vague positioning, combined with underinvestment in marketing (and inability to figure out a new motion to expand the market). Pebble reacted by trying to be all things to all people, expanding the number of products and features, drifting sharply from its roots, thereby leading to increased expenses. This given its limited financial resources, meant it was always one bad quarter away from disaster; and finally that quarter came. Pebble got to PPF but couldn’t leverage its early product success to get to MMF – it wasn’t able to figure out the right market to expand to (and devise a product for the market), nor figure out an effective go to market motion that would help it access that market.

1B.4/ The nature of PMF differs from company to company

The journey to PMF is sometimes rapid (Tinder, Youtube in months) but mostly slow grind (~2 years typically for those who achieve, but for Airtable, Figma, Notion it took 4+ years). Lenny Rachitsky has a couple of good essays on the time to PMF in B2C and B2B (both paywalled, but you can check this public tweetthread) on the time to PMF. He found that for the top companies, 80-90% got to PMF in 18-24 months, but there are a few outliers (like Notion, Figma, Miro etc.) who took a long time. His podcast episode with Jen Abel of GTM consulting shop Jjellyfish came up with a very interesting insight around which kind of companies (especially relevant for B2B) get to PMF faster. Jen’s theory is that companies like Vanta, Github which start with the market / problem first and then create a product to solve the problem tend to get to PMF faster “versus an Airtable and a Figma that I think started with a technical insight and then were trying to find their market.” The latter approach is riskier but has more uncapped upside per Jen Abel.

Just as companies differ on the time to PMF, they also differ on how they experience it. For the ‘lightning in a bottle’ PMF candidates (Lenny Rachitsky’s evocative phrase), it comes with everything breaking all at once.

- For security tech co Verkada, the cofounder Filip Kaliszan says: “We were barely keeping up with production. We had to scale all the systems. A lot of things had to happen in the span of the next 12-18 months in order to deliver on everything that customers were hoping the solution was going to do for them.“

- For Patreon, cofounder Samuel Yam says: “We felt we had PMF right after we launched with [co-founder] Jack [Conte]’s music video on YouTube and patrons and creators started writing in. I’d never seen that level of passion and immediate resonance.”

For most others, it wasn’t as dramatic with everything breaking. It was gradual.

- For incident management co PagerDuty, cofounder Alex Solomon says, “I can’t recall a specific moment in time when it clicked and we said we had product-market fit. Instead, it was more of a transition where our confidence that we had reached PMF grew over time. Throughout 2010 and 2011, we saw exponential month over month growth… I believe we hit $1m in ARR sometime in 2011). By the middle of 2011, we felt pretty confident we had product-market fit.”

- Consumer durables co Atomberg, which is a B2C play today, got to PMF initially in the B2B space. Their first product was ceiling fans with a BLDC motor (Brushless Direct Current). This was more energy-efficient than a normal fan, but also more expensive. They tried the consumer route, but got success initially in the business segment. As Arindam Paul, their Chief Business Officer says: “The ceramic tiles industry is concentrated in two districts in Gujarat, Thangadh and Morbi. In this industry they used to dry these ceramic tiles, under fans. So, there’ll be these huge sheds, and every shed will have some 500-1000 fans. These fans will be running 24/7 trying to dry the ceramic. Electricity was their main raw material cost. It was a pretty clustered industry. So, the moment you go into one of the factories, you do a proof of concept there, word of mouth spreads like anything in that segment. And there we figured out our early PMF. In fact, for the first one year, 60-70% of our revenue used to come from this industry alone.”

The Atomberg story of winning one category and one channel, and then slowly replicating the success across other categories is very common. You start with zero fit, and then slowly get to a strong fit for a category or segment. Superhuman similarly initially “found pockets of PMF with specific segments of founders, managers, executives, and business development professionals.” (More on this in the next section). PMF is thus a continuum of fits, from none at one end, to strong fit in one customer segment in the middle, to a universal fit across all segments, at the other end (e.g., ChatGPT right now).

PMF is also not permanent. It is not one and done. Just as you got to PMF on the back of great product love and relevance, figured out a great motion around a hero channel, and a compelling message, a shift in these can reduce your fit or cause it to disappear altogether.

- Chegg and StackOverflow saw their product relevance disappear with ChatGPT (loss of PPF and thus PMF)

- Edtech unicorns Unacademy and Vedantu lost MMF, and thus PMF, when they saw their Cost of Customer Acquisition (CAC) shoot up dramatically as demand eased for online classes post COVID, and they had to wrestle with opening physical centres, which increased their cost base and led to a sharp decline in unit economics.

1B.5/ How founders view PMF

A common theme that emerged across my conversations with Indian founders, and one that surprised me, was that several founders, including the ones who were successful, did not explicitly think about PMF and work towards achieving it. This doesn’t mean they had no understanding of PMF, or didn’t acknowledge its importance. It is that they didn’t track PMF, and progress on PMF, as overtly they would track a metric such as retention or CAC (Cost of Customer Acquisition). Instead, it seemed that founders aim for product love, and then solve for growth, hoping to hit the milestones for the next round of funding. As I shared above, most of these were Indian founders, but a few of the non-Indian founders I spoke to also identified with this sentiment.

These founders saw PMF as an outcome or byproduct of their efforts on generating product love and working towards sustainable growth. Interestingly, we can see product love as a parallel to the concept of PPF or Product to Problem Fit, and growth + retention + unit economics as parallel to MMF, or Motion to Market Fit. Effectively, both VCs and founders are coming at the same theme, albeit from different ends. To summarise, it seems that founders see PMF as an abstraction layer over ‘growth with high retention’. The best founders make sure that it is sustainable growth or growth with high retention, supported by good unit economics. In this regard, a shorthand acronym I recommend that founders keep in mind as a proxy for PMF is GRUE = Growth with Retention and Unit Economics. PMF = GRUE effectively. If you understand that much and that is the only takeaway from this piece, I will be happy!

If founders don’t track PMF or PMF metrics actively then how do they know they have hit PMF? The one common theme that comes through in conversation with founders or research is that when founders see increased pull from their customers, or strong inbounds, with constant or low marketing efforts, then it is a sign of PMF. Here is Calvin French-Owen, the cofounder of analytics startup Segment (acquired by Twilio for $3.2b in 2020): “The biggest difference between our ideas pre-PMF vs. when we found it was this feeling of pull. Before we had any sort of fit, it always felt like we had to push our ideas on other people. We had to nag people to use the product. When we hit PMF, we started feeling ‘pull’ for the first time.” Allied to this is increased inbounds, or organic traffic led by word of mouth / referrals. These are all qualitative and quantitative signals that help the founder intuit that they are hitting PMF.

1B/ TLDR

This section defines PMF as a combination of two sequential fits, PPF and MMF. It says PMF = PPF + MMF. First, a startup must validate that its product effectively solves a real problem for a defined set of users (PPF), and then find a scalable, repeatable go-to-market motion to reach and retain those users (MMF). Two Case studies illustrate these concepts. Front exemplifies a textbook path to PMF—starting with a focused product, close user feedback, and a content-led GTM motion that scaled efficiently. Pebble, by contrast, shows how early traction and product love (PPF) can still result in failure if the GTM motion falters, highlighting the dangers of weak positioning, unfocused expansion, and underinvestment in marketing.

The section also unpacks how PMF plays out differently across business models such as marketplaces, media, and how it varies in tempo, from ‘lightning in a bottle’ PMF to slow grind PMF. PMF, importantly, is not a one-time milestone. It can erode due to shifts in product relevance, market demand, or cost structures. Interestingly, many founders don’t explicitly track PMF. Instead, they focus on product love and growth, treating PMF as a byproduct of growth and retention. I propose a helpful shorthand: GRUE (Growth with Retention and Unit Economics) as a proxy for PMF. Ultimately, PMF often reveals itself through unmistakable signs of customer pull—organic growth, word-of-mouth, and inbound demand—all pointing to a product that truly resonates with its market.

1C/ Deepdiving into PPF = Product to Problem Fit

1C.1/ Understanding PPF

PPF or Product to Problem Fit (also referred to as Problem-Solution Fit) is achieved when you see that your product consistently solves the customers’ problem, and removes their pain. Ideally it should solve the problem for all customers who have a similar pain. If it is inconsistent, i.e., some of the people with the pain see their problem solved, but others don’t, then your product isn’t addressing the problem consistently. You haven’t yet hit Product to Problem Fit (PPF hereonwards), or at least not a strong PPF yet. If this is so, then you can then identify the customer segments or types where you have strong PPF and figure out why your product works better with those. Subsequently you can choose one of two directions – iterate and improve the product to make it a complete product addressing all customer segments, or look for more such customer segments where you have strong PPF, and focus your marketing around this limited but highly satisfied consumer set.

A fictional example: say you are a founder trying to solve for acne and you find that your product solves acne for some users, but not all, then you still don’t have PPF. You then need to dive deeper into understanding why some customers are seeing success, and why some are not. For instance it could be that some customers with oily skin are seeing success, or those with forehead acne are not, or teenagers are, but adults are not, and so on. You can then develop a hypothesis for why you are seeing success with some but not others. You can then choose to iterate on the product formulation to try and better solve all customers’ problems. Or you can say that you are happy with the customer set whose problems are being addressed, and focus on them, but sharply define your message that it is only for a subset of acne users.

Now, a real-life example of how PPF works. Early in their journey, Indian home services marketplace Urban Company found that the people who experienced their service through a marketplace (where they connected buyers and sellers of services and took a cut) had lower CSAT (customer satisfaction) scores, whereas those they served directly via their full stack service offering saw higher CSAT scores. And they found that specific personas, like working women and new mothers needing home beauty care, saw the highest CSAT scores and repeats. Clearly they had better PPF on the full-stack services side, and specifically in the home beauty care segment. And that is when they decided that they have to drop the marketplace and focus on owning the experience, and figure out more categories like home beauty care where people need it so badly.

That said, just as PMF, it is worth noting that PPF too is not a one-and-done thing. Rather, it’s a continuum, ranging from none at one end to Delta 4 PPF on the other. ‘Delta 4’ is a concept I borrowed from Kunal Shah, the founder of Indian lending startup CRED. A product is Delta 4 vs its competition if its score of efficiency on a scale of 10, is four points higher (delta = difference). Take the act of booking an airline ticket in person or hailing a street cab vs booking it online, or using Uber. Clearly online / Uber will be 8 or 9 on a 10-point efficiency scale (this is a subjective score), while booking it physically or hailing it on the street will be 3 or 4 on 10. The difference between the two is the Delta. A Delta 4 product per Kunal is

- bragworthy (you can’t stop talking about it, like ChatGPT)

- irreversible (even if you can’t use it for some time, you will never go back to the old way),

- and has high tolerance (you will put up with minor niggles and awkwardness while using it).

To clarify, very few products or categories have Delta 4 PPF. The last product that had Delta 4 PPF in India was likely Zepto / QCommerce, and globally perhaps ChatGPT / GenAI. In all likelihood you will see a range of fits, across different consumers, Delta 4 for some, and perhaps only Delta 2 or Delta 3 fits for others (stretching the concept). That is where you start digging into to understand why a select set of customers find your product attractive and must have, and then either a) rework your product so it can be Delta 4 for all, or at least Delta 3 for all, or b) focus on targeting the limited audience for whom it has Delta 4 appeal.

1C.2/ There are three Ps to keep in mind to get to PPF

The first two Ps are of course Problem and Product. The third P is persona, or really who has the problem. This is nothing but the customer segment. The term Persona, also used in the context of Ideal Customer Persona, or ICP, emerged from the world of B2B. When you are selling to a company, there can be different buyer personas that you need to pitch to and satisfy, e.g., there is one who or whose team needs it, but then there is another one who has the budget, and there is another who approves it, and so on. Clarity around your persona matters hugely in both B2C and B2B, but in B2B there is the added complexity of multiple personas that you have to cater to. EdTech is the one B2C category I could readily think of (am sure there are others) where there could be two legitimate personas – the child, who is the user, and the parent who is the buyer. The more these personas collapse into one person, the easier it is to generate a sale, typically, as you have to worry about fewer fits.

A quick two paras on the other Ps.

Problem: There is a reason I used the word problem (in PPF), and not, say, idea. As you will read in the next chapter (The Pick), it is far better to pick a problem and then explore it deeply, than jump to a solution and build the product right away. You want to immerse yourself in the problem space a bit before you jump into solutioning and committing yourself to an approach with its attendant implications. You may ask, with AI etc., isn’t the cost of building out a product low? Well, yes, but a product buildout comes with commitments and tradeoffs (around database architecture, feature sets, design paths etc.) and to reinforce those, you will also end up hiring or designing your org accordingly. That is a lot of commitment (and costs) to have very early on. Hence jumping into product creation without exploring the problem is something you ideally want to avoid.

Product: The best companies define their product loosely, as a broad solution around a large, compelling problem that customers are facing. They are intentional around shifting / transforming the product format to changing technological trends. For instance, Adobe and Microsoft both changed their product format from CD-ROM to cloud subscriptions. In this regard, this quote by Michael Bloomberg, who founded the eponymous $12b revenue financial information business is instructive. From his autobiography (italics in the below quote is mine): “Kodak thought that they were in the camera and film business instead of the photography business. The digital photography revolution passed them by. At Bloomberg, we got out of the business of building physical computers as soon as PCs began taking off. We knew our core product was data and analytics, not hardware. Do not make the mistake of confusing your product for the device that delivers it.”

Another point to note is that when you build out your product it doesn’t need to be complete or final. A minimum viable product or MVP is enough. What matters is that the MVP is able to address the biggest pain point the intended customer has. Once you see that it is able to address the core issue, then you add other features / bells and whistles. Here, I am reminded of an Annie Duke podcast where she describes an Astro Teller framework: ‘Focus on the monkey, not the pedestal’. If you are trying to train a monkey to juggle flaming torches on a pedestal in the town square, then work on the harder thing, that is, training the monkey, first. We have been building pedestals for centuries and we know we can build it. Hell, we can use a wooden block as a pedestal if needed. But the “thing that might be a bottleneck to unlocking the whole system is actually, can you train this monkey to juggle the flaming torches?” TLDR: Break down your assumptions about PPF into modular components and test the hard things first.

In fact, strictly speaking, you don’t need to build out the product too. For its first few customers, compliance automation startup Vanta was a spreadsheet. They didn’t write a single line of code till they determined that the SOC2 license process could be productisable. It was no different at Indian fashion ecommerce behemoth Meesho, which ran on google sheets and whatsapp till the founders determined this could be scaled.

Source: Twitter / X

As I shared above, with AI it is easy to create and change code too, but your architecture, core feature set, tradeoffs and the org structure needed to support the product are now committed, and you are locked in to a specific solution.

1C.3/ Two clarifications: PPF is not PMF, and it is not one and done

A common misinterpretation I see founders make is confusing PPF for PMF. Remember that PPF is only concerned with whether the product addresses the problems of a certain consumer segment or not; it excludes the market part of it (product scaling to reach a sizable market). I highlight this because this misinterpretation comes up repeatedly in several definitions of PMF that I have encountered. This is especially true for founders. For instance take this PMF definition I heard from a founder who I will not identify here: “PMF for me is when customers are asked, how disappointed will you be if this product or service doesn’t exist from tomorrow, and they rate the disappointment on a scale of one to 10 as at least 8 on 10. You want to be closer to 10 on 10, but at least 8 on 10 is somewhere you found PMF…if I’m very disappointed that the product is out of the market, I would give 10 on 10 and would be screaming, shouting, unhappy trying to grab it if someone is taking it away from my hand. That’s product market fit.” Clearly, this is more a definition of PPF than PMF. That said, I can understand why founders think like this. Most founders are drawn to start up to build a great product that solves a deep customer problem, and hence to have validation of their effort via customer feedback or signals of love, is extremely meaningful for them.

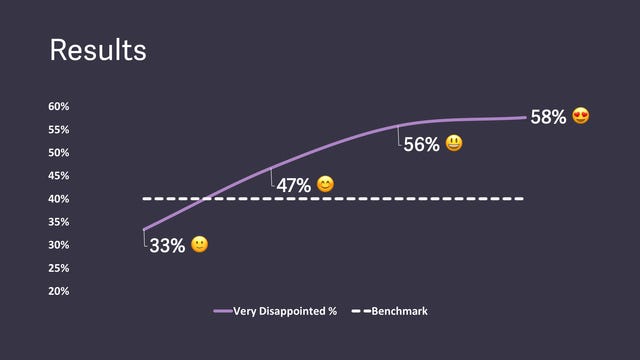

It is interesting that the above (mis)interpretation also extends to one of the most popular markers of PMF – the Sean Ellis Test. The test, conceived by growth marketer Sean Ellis, says that if more than 40% or more reply ‘very disappointed’ to your question on ‘How would you feel if you could no longer use the product?’ then you have hit PMF. The test, which was first introduced to the world in 2009, got a fresh lease of life recently when Rahul Vohra, the cofounder of email app Superhuman, wrote about how he used the Sean Ellis Test to iterate to ‘PMF’. I hold that the test is a good measure, but of PPF, and not PMF. This is because the test only measures how your existing users perceive the product, and not how to reliably, economically acquire a sizable number of customers, which is a key aspect of PMF. It ignores the market aspect of PMF. It is effectively a measure of product love, and thus of PPF.

Other measures of product love, and thus of PPF, beyond the Sean Ellis test include

- for B2C:

- High engagement rates, DAU / MAU > 25% (Andrew Chen)

- High retention rates in the early customer base; say the retention curve flatlines at 25% or higher after 180 days for Consumer Social, and 40%+ after D180 for Consumer SaaS (Lenny Rachitsky).

- For Snap, when Jeremy Liew of Lightspeed led the preseed round, they had 50% DAU to MAU ratio (Daily Active Users to Monthly Active Users) and 50% D30 (50% of installs remained active after a month) (Source). These are of course exceptional metrics, as befits an exceptional product like Snap. Even a third of these would be a sign of strong PPF.

- for B2B:

- Low churn rates in the early cohort is a good signal: <5% logo churn for SMB SaaS, <2–3% for mid-market, <1% for enterprise SaaS per Christoph Janz of PointNine Capital.

- Another would be high speed through the funnel, or low time to contract since the first meeting: 30-45 days for SMB, 2-3 months for midmarket, 6-9 months for enterprise (Source: Christoph Janz).

- Another sign of PPF for B2B companies would be strong organic referrals.

It is also worth remembering that product love, or PPF, is not permanent. PayTM hit extreme PPF (and clearly PMF) with its digital wallet product, but once UPI arrived, the digital wallet product emerged as a relatively inferior product. Before Uber arrived in India, Meru Cabs (a call for cab or radio taxi service) was a hugely popular high PPF product. But once Ola and Uber started services in India, Meru’s PPF was no longer as strong. Similarly Clubhouse had extreme PPF, but when COVID cleared and we started heading outside, its PPF disappeared. PPF can thus change with a changed context or competition from a new product better solves the customer’s problems.

1C.4/ PPF failure modes

Why do startups not achieve PPF? There are two common failure modes. The first is believing you have PPF when you don’t, and then spending to acquire more consumers who turn away from a failing product, and the startup eventually running out of money. Given there are metrics / thumbrules to estimate PPF as we shared earlier such as Sean Ellis Test, retention, speed of adoption / willingness to sign up for pilots etc., estimating strength of PPF shouldn’t be hard, and this failure mode shouldn’t happen. Yet, it does. Founders end up self-deluding themselves that they have PPF out of a refusal to acknowledge reality.

The second failure mode is not acting to address the issue of weak PPF. This could happen through one of two ways. The first by iterating and improving on the product to arrive at a better fit. The second by iterating on (shifting or narrowing) the customer segment, so as to improve product to problem fit. To understand where to focus – iterate on product, or customer segment – it is best to start with the metrics. While evaluating the metrics, you could and should disaggregate / de-average these across various segments, because early on in the history of the product and the co, it is unlikely that you will get blowout numbers, or meet the benchmark metrics across the entire segment. If you are able to see only a subset of the targetable customer segment meet the benchmark metrics signifying product love, this is acceptable. This aspect – that you will typically have product love from a narrow but targetable customer segment (and not the entire target universe) is important and holds for both B2B and B2C apps / brands as well. Two examples illustrating the above follow, the first on product iteration, the second on customer segment iteration.

Grocery etailer Instacart saw product love from a narrow set of customers, specifically those who were concerned with speed of delivery. As cofounder Max Mullen puts it: “We found product-market fit very early on with people who wanted groceries delivered as soon as possible and didn’t care which store they came from. This made us feel like we had achieved product-market fit [sic] but it was only with a small sub-segment of customers. The average customer wanted to shop from their favorite grocery store. So, we formed partnerships with top retailers. As a result, customers started to seek us out and word of mouth grew. We then signed more partnerships, reached a larger scale with customers, and in turn attracted more partners.”

With regards to the second type, customer segment iteration, the case study of email app Superhuman is a good example. Superhuman used the Sean Ellis Test to find that they only had 22% users who thought they would be very disappointed if the app failed to exist. When they narrowed down the user base to Founders / Managers / Biz Dev or Sales execs, they saw this score jump to 32%. They looked at the feedback from these three personas, ignoring others like Engineers, Customer Success folks, and worked to address the concerns of these three personas, such as lack of a mobile app. With these interventions, and narrowing the customer segment they were targeting, they started to see the Ellis score improve.

(Source: Link)

There is a lot more here we will go into at length in the PPF chapter (to be published) but this example gives you an idea of how you can both narrow the customer segment, and then iterate to improve the product to enhance the fit.

1C/ TLDR

This section deep dives into Product to Problem Fit (PPF), the first foundational step toward Product Market Fit. PPF is achieved when your product consistently solves a real pain point for the customer segment. Inconsistency signals weak fit, prompting founders to either improve the product or sharpen their focus on segments where strong fit exists. PPF is best seen as a continuum from weak to strong, with exceptional products achieving what Kunal Shah calls “Delta 4” fit: so transformative they become bragworthy, irreversible, and high-tolerance.

To reach PPF, founders must focus on three Ps: the Problem (deeply understood before building), the Product (designed flexibly, often starting with an MVP), and the Persona (the customer segment experiencing the problem). A tight understanding of all three is essential. Importantly, PPF is not the same as PMF as it captures product love, not scalability, and is often mistaken for the latter. Founders and even popular metrics like the Sean Ellis Test often conflate PPF with PMF. But while high user engagement or retention reflects product love, it does not guarantee market-scale traction. Moreover, PPF is not static. As markets evolve or new competitors emerge, what once felt like strong fit may erode, as seen in cases like PayTM Wallet or Clubhouse.

Common PPF failure modes include prematurely scaling before true PPF is achieved, or failing to act on weak fit by not iterating on the product or targeting the right segment. Case studies like Instacart and Superhuman illustrate how founders can deepen fit by refining product features or narrowing the customer focus. In short, PPF is where sustainable product love begins; knowing how to assess and iterate towards it is critical for long-term success.

1D/ Deepdiving into MMF = Motion to Market Fit

1D.1/ Understanding MMF

Now that you have PPF, the next step is to work towards MMF or Motion to Market Fit.

- Motion here is short for go-to-market Motion. To repeat, go-to-market, or GTM, as it is referred to in the startup world, consists of the set of activities and capabilities that enable you to take the product to the customer, or bring a customer to the product. It is what the analog world refers to as Sales & Marketing.

- Market refers to a set of clearly defined, or definable, buyers with similar needs and similar purchase behaviour. Thus, founders need to see signs of a reasonably homogeneous set of customers, with similar problems and characteristics, and some evidence that there is a large number of these customers.

If PPF demonstrates that your product reliably solves the problem for a defined segment of customers, then MMF is about acquiring a large number of lookalikes of that segment (i.e., ‘market’) in a scalable, repeatable, and sustainable fashion (i.e., ‘motion). This is the motion to market fit or MMF.

The adjectives to describe motion – scalable, repeatable, and sustainable – were carefully chosen. These constitute the qualitative criteria by which to judge a GTM motion which enables customer acquisition and thereby generates revenue. A GTM motion, and thereby revenue generation, which does not meet these criteria will not lead you to MMF. To clarify these three criteria better

- Scalable: If you spend $10k to generate $50k, then with a $20k budget, you will generate $100k, and so on; of course at some point with increasing spends, you will hit channel saturation and the same ratio may not hold.

- Repeatable: GTM motion can be done repeatedly to acquire customers and realise revenue. Thus you will not run out of a market; there is some predictability of revenue.

- Sustainable: From a financial point of view. The revenue should be unit economic positive, ideally covering all variable costs of acquiring that revenue including the cost of goods sold, and ideally all direct variable costs incurred in realising the revenue (including performance marketing costs).

Ideally, the customers you are acquiring are similar to the customers you acquired during the PPF phase, i.e., engaged customers whose problems are getting solved through the product. You are seeing continuing retention levels as before (or at least not seeing a drop).

We now know what kind of motion we want. Now, let us dive deeper and understand (GTM) motion better. GTM has three broad components

- Persona: we covered this in the previous section. This is essentially the paying customer, but in B2B, and in certain cases in B2C, the payer and user will differ.

- Channel: How will you reach your customer persona? This could be, for instance, performance marketing, event-led reachouts, or top-down SDR-led outreach.

- Message: What is the message you share when you reach the customer, or in order to attract the customer? The message typically has two parts – benefit to the customer, and product proposition ( conditions around usage, such as 1- year warranty, free installation or onboarding etc.)

Here are two examples to clarify the above components better:

- B2C GTM motion for a pet food company: I will reach dog owners residing in Gurgaon (persona) by sponsoring or installing banners (message in the banner) in dog parks and societies (offline marketing channel).

- B2B GTM motion for a martech SaaS co: I will reach marketers who spend at least ₹1cr ($125k) a year on digital marketing (persona) via inbound (channel) using content marketing (channel, message)

1D.2/ Iterating to MMF

Uncomfortably narrow personas addressed by one hero channel through a sharp message is how first-time MMF is achieved. Let us unpack this.

- Narrow personas: The narrower your persona, the easier it will be to leverage a channel to reach them, and craft the message that will get them to try the product, and the better your product will be in satisfying them. For instance, Gong, a sales call listening and insights company, narrowed their ICP to B2B software companies in North America selling in English, $1-100k annual contract value transactions via videocalls. It was that specific. This narrowed their ICP but made the targeting and messaging sharper.

- Hero channel: I have noticed that companies which get to MMF and hence PMF faster, often have 1 dominant channel. Here is Karan Bajaj, who founded kids coding co WhiteHatJr, and rapidly grew, and then exited it successfully for $300m, all within two years: “I think my biggest insight is one or two distribution mediums work. Once you figure out those one or two distribution mediums that work, you should go blitz scale on them. And just let go of everything else. In my writing days, it became very clear that Amazon advertising is working. And I would just go and really spend my own money to scale them. In WhiteHat Jr., for example, very early, we figured out that Facebook was working, we built an entire ₹100 crores ($12m) a month business just on Facebook advertising and referrals, right? And we did nothing else. And so, I think with distribution, what I’ve seen is that every brand, which is good, we’ll figure out one or two mediums that really hit a chord, and then you should just scale them like crazy. Versus like diversifying too much.”

- Sharp message: The better your communication (ad / mail / collateral) highlights the benefit and value your product will add to their customer’s lives, the stronger it will land. Retool, which helps companies build internal software tools, initially described itself as ‘excel with higher order primitives’. While this was perhaps how the founders saw their product (from a supply-side perspective), this made no sense to the prospective customer. It was only when they shifted the message to ‘helping companies build internal software’ that they started seeing responses.

When you are striving towards MMF, you are continuously iterating on persona, channel, message, and product. Think of this as fiddling with different dials and knobs to hit high fidelity. That said, there is a hierarchy of iteration. It’s easier to iterate on the Message first, then if that is not working you move to change the Channel, and then if that also is not working finally the Persona, which also means you will in all likelihood have to modify the Product too. This graphic below should help.

To clarify the above:

When you change the Message, you’re adjusting the language used across different communication materials—like Retool did. This includes ads, website copy, email campaigns, brochures, and other marketing collateral. The goal is to convey a new benefit or value proposition—these are the two key parts of the Message.

A Channel change, on the other hand, means shifting how you reach customers. For example, moving from performance marketing alone to a mix of performance and display ads, or from email campaigns to event-driven outreach. Both Message and Channel are relatively easier to change and their impact is quicker to measure.

The lower layers—Product and Persona—are much harder to change. Altering the product requires more resources and time, both to implement changes and to see their effects. In fact, a product change is essentially a pivot, as it often means reworking much of what you’ve built so far.

Given that each funding round typically gives you a runway of around 18 months, and a product pivot takes 3–6 months to execute and test, you only have the capacity for at most two pivots. Realistically, you can only afford one.

Now, how long do we continue iterating? How do we know we have hit MMF? The best way is to go by the three qualitative criteria we judge GTM motion by – scalable, repeatable, unit-economic positive / sustainable. Effectively a high quality GTM motion (scalable, repeatable, sustainable) gives you revenue that is high growth, high retention, and with strong unit economics (GRUE, as we referred to it in the PMF section earlier). So, we have

- Growth: monthly double digit growth is great, but 5%+ is good.

- Retention

- B2C: flatlines at 25% or higher after D180 for Consumer Social, and 40%+ after D180 for Consumer SaaS (Lenny Rachitsky).

- B2B: 60%+ D180 for SMB/Mid-Market SaaS, 70%+ D180 for Enterprise SaaS (Lenny Rachitsky)

- Unit-economics: Cost of acquiring and serving the customer is lesser than the value of the customer = ideally CM2 positive (What is CM2+ you say?)

- B2C: say LTV:CAC ratio 3:1 as a thumbrule

- B2B: S&M costs as <50% of contribution margin, or sales yield > 1

When MMF is achieved, you have effectively hit PMF. In ‘vibe’ terms, the above metrics should also be reflected in what you see in real life: crazy demand, clear pull from the market, and customer support breaking. Marc Randolph, co-founder of Netflix: “All of a sudden we couldn’t keep up. Our previously prodigious amounts of inventory were suddenly not enough. Engagement soared, churn went dramatically down. Everything started working!”

1D.3/ MMF failure modes

Why do startups not achieve MMF?

Let us consider a scenario where a startup has strong PPF / product love. If so, what could lead to failure to achieve MMF, especially if it follows the above steps systematically?

The classic scenario is that the product has strong appeal to a small minority but you are unable to break out beyond that, and then eventually run out of money. We saw this play out in the Pebble case study. While they had strong inroads and love amongst the tech nerd / geek community, they were unable to translate this success to other groups like the fitness community. They tried to make it work with different products, but ran into strong competitors and hence couldn’t increase market share. This is a classic challenge that many Indian startups also face as they transition beyond the high-income India1 households (~10% of the ~300m households in India) which constitute the consumer engine of the Indian economy, to the wider India2 segment (~33% of total households). The India1 household is not as price-sensitive as the India2 segment. To expand into India2, you may not only have to reprice it (sachetisation is one approach) but may even have to rework it completely to make the economics of the cheaper product work. This is the classic ‘crossing the chasm’ challenge.

Venture growth investor Niren Shah, Norwest Venture Partners remarks on the challenge of operating in India: “An early product-market fit in the Indian market is not a good representation of whether you have truly achieved PMF. That’s because it has to be achieved with unit economics. We have seen people achieve early PMF. However, when they try to build some margin, break even or move closer to such a position, they have to change the pricing. While doing so, they end up changing consumer segments, which lack depth. In effect, you move away from your initial PMF and you need to rebuild.” In Niren’s definition of PMF, unlike ours, he doesn’t factor in unit economics, but what he is saying broadly corresponds to what I shared above. In India, the early product that helps you succeed, is not the product that can keep growing for you. You have to re-engineer or adapt the product to the wider market, and that means you have to find PMF all over again. Unlike the U.S., which is a wealthy and relatively homogeneous market, India has a small number of high income households. You have several distinct markets rather than one national market to find PMF in.

Another scenario is when the startup is unable to build a scalable GTM playbook, i.e., $1 spent on GTM / sales & marketing leads to $3 but increasing the spend on GTM to $3 doesn’t give you $9 but only $6. And so on. The unit economics also take a hit as you are paying more to acquire and serve a customer. The classic reason is, of course, channel saturation, where you are spending more to get customers from a channel. You now have to figure out a new channel. Performance marketing is a classic culprit – it is the only medium where there are diminishing returns to scale; the more you advertise, the higher your customer acquisition cost (CAC) is. Another possibility is that competition is high and everybody is chasing the same customers, leading to poor returns on GTM spends and worse unit economics.

Meal kit delivery service Blue Apron is a cautionary tale of how increased competition as well as intrinsic challenges with the product category can make it hard to achieve or sustain MMF, even though there is strong PPF. Once a storied unicorn, valued at $2b at its peak, Blue Apron IPO’d in 2017 but struggled since. It was sold in 2023 for $103m. What went wrong?

- No hero channel: In Q1 2017, a third of new customers came through referrals, even though referral spends were under a sixth of the marketing spend. They also spent on podcast ads, YouTube show sponsorships, and traditional ads. Clearly there was no single hero channel, even though referrals had the opportunity to be one.

- Low retention / churn: Subscription meal kits were a low retention category – human tendency to seek variety, perhaps costs, and competition all playing a role. Most estimates of their retention after a year put it from 18% to 23%. Thus about a fifth of subscribers were retained after a year.

- Poor unit economics: Meanwhile, CAC rose from $63 in 2015 to $386 by Q1’17, driven by increased competition and channel saturation. Given Blue Apron was only making 31% gross margins on an ARPU (Average Revenue Per User) of $236, equal to $75 approximately by Q1 2017, 20% retention meant a 2+ year payback period. They were spending more to acquire worse customers.

1D/ TLDR

Having achieved Product Problem Fit (PPF), the next milestone is Motion to Market Fit (MMF), where startups systematically acquire large numbers of similar customers through a scalable, repeatable, and financially sustainable Go-To-Market (GTM) motion. GTM comprises three core elements: Persona (the buyer), Channel (how you reach them), and Message (what you say).

Uncomfortably narrow personas addressed by one hero channel through a sharp message is how first-time MMF is achieved. Iteration starts with the Message (easiest to tweak), then Channel, and finally Persona and Product—both of which are resource-intensive to change. Strong MMF results in high-growth, high-retention, unit-economically sound revenue (GRUE). Benchmarks include D180 retention of 25%+ for Consumer Social, 60%+ for SMB SaaS, and healthy LTV:CAC or CM2-positive unit economics.

Failure to achieve MMF often stems from three scenarios: (1) a product beloved by a small niche but unable to scale (as with Pebble); (2) a promising early-market fit that doesn’t translate to broader segments like India2, where lower pricing and altered GTM strategies are required; or, (3) inability to scale GTM cost-effectively due to channel saturation or rising competition, as seen with Blue Apron. Despite early traction, Blue Apron suffered from lack of a hero channel, poor retention, and deteriorating unit economics due to skyrocketing CAC. MMF is about traction that scales efficiently, predictably, and profitably. When done right, it’s the bridge from product love to a growing, durable business.

1E/ Founder’s role in PMF

Let us understand the role of the founder at each of these stages: a) PPF = product to problem fit b) MMF = motion to market fit.

The first stage, PPF, includes building the MVP, getting it to customers, gauging their feedback, and then iterating on the product. The role of the founder here is to act as the Head of Product. The team translates the founder’s vision into reality; the founder leads product development, feedback, and iteration. In the case of B2C products, such as consumer apps, it is relatively easier to gauge reactions from a small beta group. In B2B, it depends. If you know the industry well, you can quickly reach out to your contacts and get feedback. If not, it can take a little longer to get quick feedback. One way is to co-create the product with your consumer, i.e., get a design partner or two aboard so you can get feedback faster. This is how EvolutionIQ, Gong etc., got started.

The key here is increasing the number of product iterations and feedback cycles to learn faster. That said, I believe the only way to get effective feedback from the customer is by seeing how they interact with the product through the process of buying and utilizing it, not by hearing them talk. Believe what they do, not what they tell.

For the next stage, MMF, the founder is testing the effectiveness of the playbook for GTM + monetisation, i.e., whether they have adopted the most efficient approach to get the product to the customer. Is the energy expended to transfer a rupee from the consumer’s wallet to yours the lowest possible? Does your product ‘hook’ as frictionlessly as possible into the customer’s product adoption and purchase processes? If there is friction, you need to change your GTM approach.

- In B2B, you are determining the optimal channel (partnerships or performance marketing or content marketing) to source pipeline, and simultaneously test the message or narrative. It helps for the founder to do a certain number of sales meetings to get first-hand customer reactions.

- In B2C it means you are determining what your most effective path for customer acquisition is – performance marketing, virality, or content. Which route gives you the best ROI on your customer acquisition investments?

In both B2B and B2C you are striving to double-down on what works best in customer trials, adoption and engagement to arrive at the playbook. Almost always, the learnings from this stage result in further product iterations and refining the value hypothesis, which later influences the growth hypothesis, and so on.

To summarise, each of the two phases has different asks of the founder. The first requires the founder to drive faster product iteration cycles to ensure that the product meets much of all customer needs, or solves the problems the product was designed for. The second needs the founder to explore various paths to take the market to a wide segment of customers, so as to determine the most energy/cost-efficient path to scaling.

1F/ Wrap

The half-constructed bridge in the pic below is such a good metaphor for (early) PMF! It is unsafe, with no side fencing, but people are using it. Apt.

Source: X / Twitter

We are now at the end of this piece, which is the introductory chapter of a playbook for founders to use to work towards PMF. Let’s revisit the key takeaways from this chapter.

First, PMF or Product Market Fit is actually two fits: the first is PPF or Product to Problem Fit, and the second is MMF or (GTM) Motion to Market Fit. PMF = PPF + MMF.

Second, when you hit PMF, you have arrived at a scalable GTM motion enabling repeatable, unit-positive acquisition of customers with high retention. A mouthful I know! But really, when you have this working, you will have high growth, with strong retention, and positive unit economics (GRUE as I termed it earlier). And, if you have achieved high growth with strong retention and positive unit economics, you have effectively achieved PMF.

Third, avoid common failure modes. The classic failure mode in PMF is pouring on the marketing dollars ahead of PPF, i.e., premature scaling before nailing. Remember, prePMF startups are a learning machine, not an earning machine. In this context, I like tech leader and entrepreneur Sidu Ponnappa’s description of the pre-PMF stage as an experimentation and search engine, one that can “search the solution space most efficiently to find PMF. Once I find PMF, then I pivot to actually building the product.” You are seeking at this point to validate that your hypotheses about the problem and the potential solution are correct – if revenue or monetisation helps you validate those hypotheses, then great, but revenue maximisation alone is not the goal prePMF. You ideally want high quality revenue – revenue that is high growth, strong retention, and positive unit economics (there I go again!). There are failure modes in PPF and MMF too, which are chiefly around not iterating enough to work towards the fit.

Finally, two bits of advice for founders

- PMF is a grind. Occasional examples of ‘lightning in a bottle’ PMF such as Twitter aside, most PMF achievements are a steady, slow grind. It is a lot of fiddling with the dials and iterating on the product / GTM elements till you hit high fidelity. Even after PMF, you then need to ensure the product is relevant and updated to every new customer set that you cater to.

- PMF is not a one-and-done thing. PMF can come and go (just ask Paytm’s Wallet team or the Clubhouse guys). At every stage of growth, your quality of Product Market Fit can change / weaken. You will then need to adjust your messaging, channel, product and persona selection and configuration to adjust for this.

1G/ Additional thoughts

1G.1 PMF is easier in B2B than B2C

Over the past years of working + interacting with founders, and helping them think through the process of getting to product-market fit (PMF), one conclusion I have come to is that PMF is relatively easier in B2B versus B2C (well, nothing in PMF is easy but relatively!). This is especially for B2B startups with top down motion as opposed to B2C. B2B startups with PLG motion fall somewhere in between (relatively easier than B2C, but harder vs B2B top down motion).

B2B startups with a top down motion have 2 advantages when it comes to PMF. One is less feedback friction, and the second is easier visibility on purchase reasons. Let us unpack these.

1/ Less feedback friction: There is direct feedback from every customer in B2B unlike B2C; and because in the early phase, the founder is selling (always!) the learning on the product is faster – the feedback / decisions can be relayed to engineering teams and the product iterates faster (Front, Retool all had superfast pace of iteration). In PLG the feedback is not always direct and hence there is learning impedance. In B2C it is even worse, as it is difficult for the founder to get feedback from most users. This is why the best B2C founders / founders of successful B2C startups, are those obsessed with talking to individual customers.

2/ Visibility on purchase reasons: Every B2B product is a painkiller; it is purchased because it is faster, better, cheaper than the competition or some alternative / workaround, and there is some resulting benefit measured through some cost, time or revenue advantage. The B2B buyer only buys your product because it confers a certain benefit / yields a certain value, and this is discoverable and addressable through specific features which can be improved upon thanks to the learning from direct conversations with the customer (see above).

On the other hand, many B2C products are vitamins, not painkillers, and often it is unclear what exactly led to the customer buying it / what benefit it conferred, e.g., Tiktok, Mokobara bags, Comet shoes. It sometimes becomes hard to understand the exact benefit or see a clear pattern of benefits emerge, and thereby build product features and GTM hooks to leverage that pattern. It’s also harder to reach out to and get feedback from the customer. Moreover, customers may be embarrassed to share the ‘true’ reason for purchasing – that it was cheaper or looked good.

Takeaway: B2C founders should budget time to speak to 3-5 customers every week. It takes ~30 minutes per customer and it is worth it. They should try and search for patterns of purchase – and track it to benefits (The JTBD framework can help – what is the job to be done in my customers life that my product is being borrowed for?). Again, don’t believe all that the customer says. Go by what they do as much, if not more than what they say. Doing great customer research is an art and a science, and it is a whole different topic altogether. Read resources like The Mom Test, keep interviewing customers, and you will get better with time.

1H/ Additional readings and references

A considerable amount of research underpins this chapter. In the early days of research when I was feeling around the structure of this chapter, I even set out to try and find and read every single definition of PMF written! For the readers who have got thus far, and want to explore PMF further, here are a few more readings you could check out.

1/ The PMF Method, by First Round Capital, is a comprehensive framework for B2B companies to work towards PMF. They opened up the framework in a post (and in a Lenny’s podcast episode) but much of the secret sauce is being reserved for an in-person program they run. I wrote about my thoughts on the framework here.

2/ First Round Capital has a series called Paths to PMF where they publish case studies of well-known startups and how they got to PMF. Recommended.

3/ Lenny Rachitsky has written extensively about PMF in his newsletters. Some particularly relevant ones include how to know if you have PMF, how long it takes to find PMF, finding PMF in B2B and PMF in B2C.

4/ James Hawkins, cofounder of product analytics platform Posthog, wrote an excellent (and long) article outlining a step by step guide to hitting PMF or product-market fit. He visualises PMF akin to a game, with 5 levels and covers how to jump levels to iterate towards PMF. More relevant for B2B / SaaS founders than B2C given James’ experience w Posthog. My only quibble with the piece is that while James describes scaling to five or more reference customers as getting to PMF, in my playbook, this is actually PPF. Repeatable scaling post five reference customers via a GTM playbook is what is truly PMF per me. But this is my opinion against his opinion + track record of building to $20m ARR.

5/ John Danner, edtech founder and angel investor, wrote some insightful pieces on PMF – notably this series which was synthesised into a comprehensive PMF playbook.

6/ I have learnt a lot from exVC David Skok’s writings on this topic. Start here for a short series on PMF.

7/ MicroVC Hustle Fund’s cofounder Elizabeth Yin has tweeted extensively on PMF, and I have learnt a lot from her perspectives. Here is a good tweet thread from her on PMF.

8/ The PMF Show by Pablo Scrugo is an excellent podcast devoted to PMF. Host Pablo Srugo of Mistral Ventures, a Canadian VC, hosts founders (not all are well-known) to talk abt their road to PMF. In Depth podcast by First Round Capital, while not exclusively about PMF, also has episodes that describe the path to PMF. In addition, do check out Unusual Ventures’ Startup Field Guide podcast (now discontinued).

If you want more recommendations around specific subtopics in PMF, or have any queries in general, please feel free to hit me up at sp@sajithpai.com!

***

Thanks to Jeevesh Saxena, Anurag Pagaria, Nachammai Savithiri, Radhika Agarwal, Gauraang Biyani, and Rohit Kaul for their deep reading and detailed feedback on the essay.

July 31, 2025 @ 12:37 pm

Although the quoted examples and the jargons around the PMF are nice, I really did not get an insight reading the entire first chapter.

The effort in explaining the hooks around PMF is good but without explaining what exactly PMF is and how you find them its useless. For someone coming from the startup/VC industry, it is a good read but again no insights which makes reading this pointless (apart from the ability to quote a few examples from the read)

August 3, 2025 @ 1:33 pm

Thanks for reading it and noted the strong feedback, Sparsh. Views like ‘pointless’, ‘useless’, and the strong language took me back. I have checked re your feedback with other readers, and all of them disagreed with your feedback, and said there was a clear definition (explained what exactly PMF is) and that it was insightful. Many of them are people who are very direct and strong-minded and won’t say something just to please me. Even on social media (twitter, LI) there is a fair amount of love for the article, and many founders have found it useful.