A frequent question that comes up in VC (venture capitalist) interviews / podcasts is around how VCs decide on investments, or rather, how they evaluate a startup or pitch.

The inevitable answer to that is that you quickly determine how the startup stacks up on three broad criteria: the team, or the quality of the founders, then the product or tech being used here, and finally the market or the opportunity that is available to tap given the business model and idea. Occasionally only two of these come up, and sometimes there is another, but the bulk of the answers are around the trifecta of team, product and market.

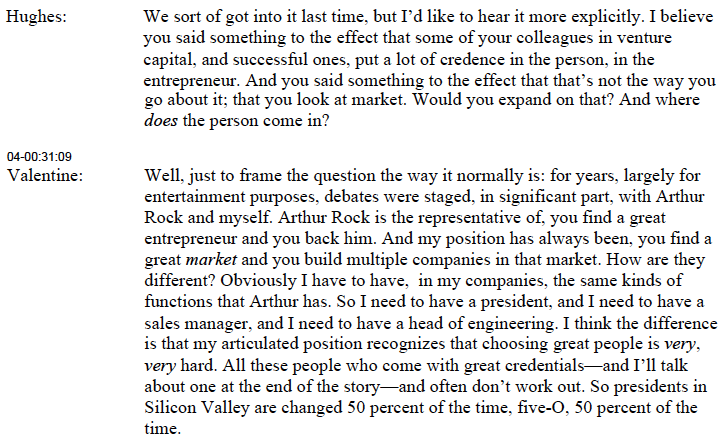

What is interesting to me is that, when evaluating the startup on these three axes, the weights assigned by each VC to the elements are rarely equal. Often one of these get stressed more – typically, the earlier the stage of investing, the more the tendency to stresss the importance of the team over the other two criteria, but this isn’t uniform, and one of the greatest venture investors of all time, the founder of Sequoia, Don Valentine in fact stressed the market over team. Another investing great, Arthur Rock, stressed the team over other elements.

The overweighting of a particular axis is also revealing of the investor’s venture investment style – whether he or she is a markets-first investor, or a team or product first investor. This preponderance for a particular axis, or the investment style matters.

It matters because at the venture stage, it is hard to assess the quality of the investment proposition objectively, unlike say in public market investing. Venture investing is largely driven by gut, belief, pattern-matching from past successes and failures. And in this context, your tendency for over-reliance on one axis can matter immensely on whether you say yes or no to a specific pitch. Two VCs can evaluate the same pitch and can arrive at a difference conclusion basis their investment style.

More on this soon. First, I want to talk about these styles.

Investment trifecta and the three investment styles.

I came across a fascinating paragraph in a book that I was reading on the history of venture capital (‘VC: An American History’), which really set me off on a venture history rabbit hole and eventually led to this blog.

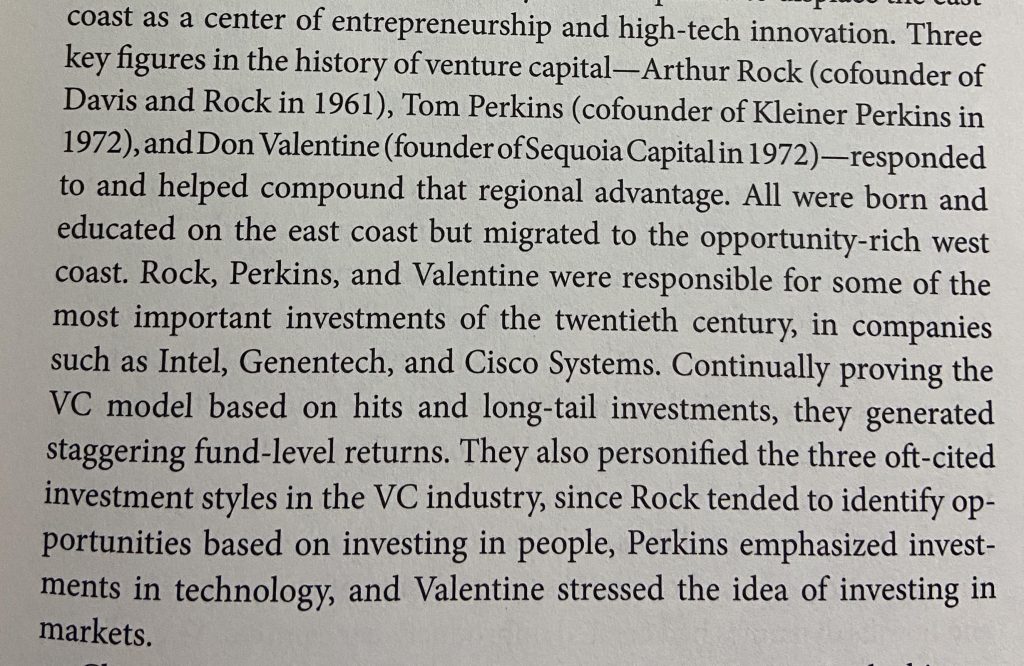

It is interesting that this was a fairly important debate as the venture industry evolved in the 70s and 80s in the U.S., and Don Valentine, Tom Perkins and Arthur Rock emerged at the vanguard of this new investing practice.

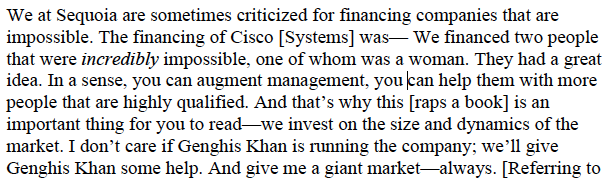

Don Valentine was asked this in 2009 and he responded:

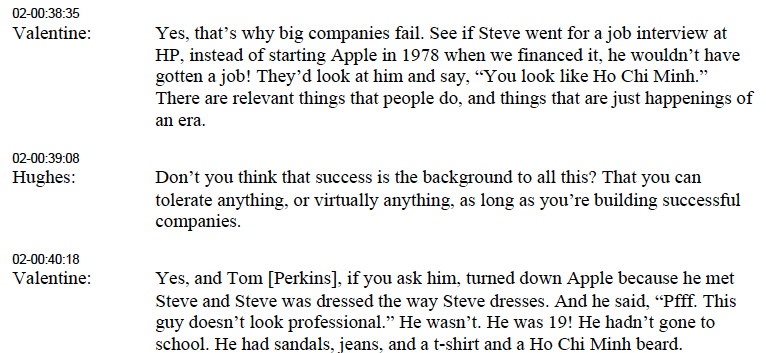

It is interesting to hear how Don Valentine describes his encounter with Steve Jobs, including how Tom Perkins (of what eventually became Kleiner Perkins Caufield Byers or KPCB and now Kleiner Perkins) turn Steve Jobs down. Don Valentine invested in the seed round in Apple.

Effectively what Don Valentine is saying is that if you are markets-first you will learn to live with founders who may not fit the market’s perception of a rockstar founder (such as from a non elite school or introverted etc).

Why does Valentine not care as much about people as other investors do? Well, his belief is that great people are hard to find or select. And a great and growing market can always make up for the seemingly ‘non-great’ but effective people.

All of the above images from this oral history of Don Valentine.

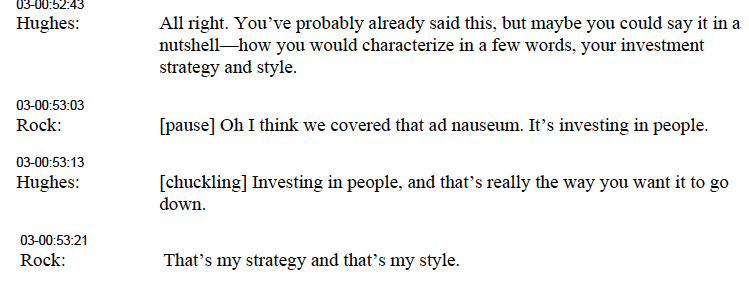

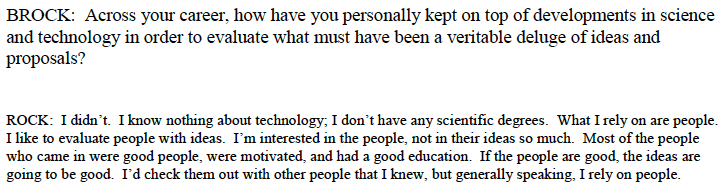

Let us look now at Arthur Rock, again one of the great investors (Intel, Apple etc) of that era, who is known for his investment style of team-first or people-first.

Arthur Rock says:

Above image from this oral history of Arthur Rock.

In another oral history, Arthur Rock stresses “I’m interested in the people, not the ideas so much.”

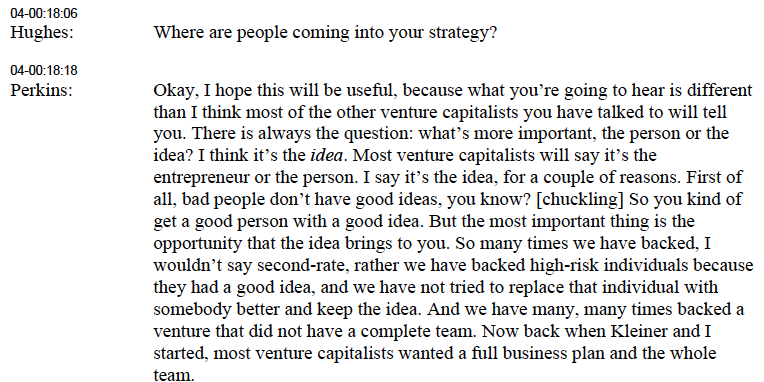

It is interesting now to get the perspective of Tom Perkins (of Kleiner Perkins), who holds the exact opposite view – ideas, not people.

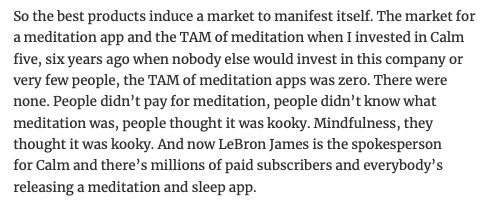

People-first or market-first approaches are intuitive to grasp; however product-first approaches (and here product = idea / technology) aren’t and it is useful for us to dwell on how product matters. The broad thesis is that a great product / product idea can meet dormant or suppressed needs and create a massive market.

Let us hear it from Tom Perkins first.

The best example of how a product can create a market is perhaps Uber. In the early days it wasn’t entirely apparent how big the market for Uber was. There was a famous debate between NYU Professor Ashwath Damodaran and Benchmark’s Bill Gurley, who led their Series A in Uber about the Total Addressable Market for Uber. Would Uber get a share of the cab market (if so it was overvalued) or was it really competing for total miles which meant it could replace private car market and public transport too (and hence undervalued)? Gurley won the debate handily, and the entire Uber deal was a bet on the belief that a superior product would create a massive market.

Jason Calacanis explains this well – TAM here stands for Total Addressable Market, lingo in the startup world for potential market size.

Phew!

So what kind of an investor are you?

At the risk of repetition, I don’t think anyone exclusively relies on only one of the three axes. Rather they filter the proposition or startup pitch on all three axes, but overweight one of the axes. Given the nature of the venture business, the earlier the stage at which the investor plays, the more the likelihood that they will prefer the people-first approach. I hazard that people-first investors will account for the largest type of seed investors, followed by product-first and then finally market-first investors.

Let us look at these one by one.

Market-first: For anyone leaning towards the market-first approach, you need to evaluate the opportunity not from today’s TAM but what it could realistically be. This post from Benedict Evans on how to think about market size expresses it well.

Another way to look at TAM, which I prefer, is to see the product offering through the jobs-to-be-done framework, i.e., the customer is hiring the product to solve a problem or two for her, e.g. a virtual makeup app that smartens up your appearance digitally for a zoom call is competing with expensive foundation and lipstick, e.g., like the TeleBeauty app from Shiseido. If Work From Home becomes semi-permanent then such an app is not a cool toy so much as a beauty products replacement. Its TAM is potentially a large percentage of the beauty industry.

Market-first investors or product first investors should also not overthink team qualifications. The very fact that the market opportunity is large affords them the ability to back Ho Chi Minhs and Genghis Khans (as Don Valentine put it). They can err on the side of the team or product given that they have put their eggs in the market bucket. Also, market opportunity is the only element that is fixed; the others – product and team are constantly evolving. Hence an incredibly large opportunity will pull the founders to evolve, help raise funds and build a fantastic product and so on.

People-first: People or team-first investors are backing great founders with a high degree of conviction. The team or people-first philosophy is expressed in inimitable fashion by Georges Doriot, one of the founding fathers of venture capital – “Always consider investing in a grade-A man with a grade-B idea. Never invest in a grade-B man with a grade-A idea.”

For people-first investors it isn’t that the market or product doesn’t matter. Of course it matters. But they believe that the founders will continually strive to push the venture in the direction of the biggest market they can aspire for, with the best product that they can build. Arthur Rock says “If you can find good people, they can always change the product. Nearly every mistake I’ve made has been I picked the wrong people, not the wrong idea.”

Amongst all the three styles, it is people-first investors who will be willing to invest in a copycat idea or a situation like a founder entering a large and promising market late without a clear technological edge. They believe in the founder and have the conviction and confidence that the founder will rise to the challenge.

It helps to have a large library of past patterns that you can try and match present founders to. And that does help them bet on investment opportunities that their peers following the market-first or product-first styles won’t touch.

Product-first: Product or idea or technology-first investors, as exemplified by Tom Perkins of KPCB or Vinod Khosla of Khosla Ventures, give a great degree of weight to the technology, that is, the specific route the entrepreneur is taking to address the market. Here is a quote by Vinod Khosla that articulates this well – “In the end, what really interests me is the technology. I don’t even invest in businesses where six other people have the same technology. The idea is how can you turn a technology advantage into a business advantage? It’s much more like playing a chess game than it is investing. It is strategic, it depends how much you can help the company.”

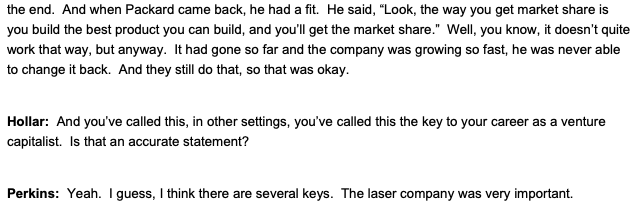

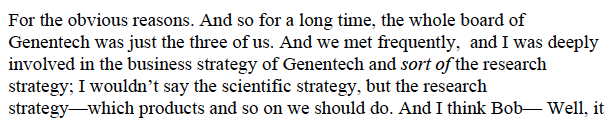

Clearly this type of investing requires deep subject matter knowledge. Here is Tom Perkins on his role at Genentech, his most successful investment.

This is typically the style that is practices by mid-career professionals shifting from technical roles to the venture industry. Their deep subject matter understanding helps them evaluate which approach is promising. All of deep tech, healthcare and biotech investing sees this approach.

So what kind of a venture investor am I?

When I look at my approach to evaluating startup pitches, then I find myself firmly in the market-first camp. It is both a bent of personality – instinctive preference for the market-first approach – as well as the fact that I am new to venture and tech, and hence don’t have enough pattern recognition for evaluating founders or product / tech as well, thereby forcing me to go full hog on using market as the primary evaluation criteria.

That said, and as I shared earlier, none of us are exclusively relying only on looking at one of the criteria, say team, and entirely ignoring the other two. The product-first investor wants to make sure the team has the technical chops to deliver and the people-first investor prefers a great team chasing a bigger market. Still there is a preferred axis you like to rest on, and for me that is the market.

So what kind of a venture investor are you?

May 15, 2020 @ 5:18 pm

Worth Reading. Must for every entrepreneur, to understand investor mind!

May 17, 2020 @ 10:56 am

Thanks for your blog posts, really well thought our and articulated with superb specific examples as always.

Also thanks for all the content you share on twitter, love reading your insights and thought provoking ideas in thr venture capital space. Its a fascinating rabbit hole, which we ourselves are also learning about.

Thank you once again for your generosity.

May 24, 2020 @ 11:43 am

Thank you for your kind words, Vaibhav.

August 3, 2020 @ 8:06 pm

A very good read with amazing examples.